Review and Prospect of Hot Issues in Semiconductor Application Market in 2012

Semiconductor applications are global industries. In 2011, the European debt crisis was dragged down, and imports and exports fell sharply; 2012 will undoubtedly be a challenging year for the semiconductor industry; some global macroeconomic issues will not only affect the semiconductor industry, but also It has a negative impact on the global economy.

Semiconductor applications are global industries. In 2011, the European debt crisis was dragged down, and imports and exports fell sharply; 2012 will undoubtedly be a challenging year for the semiconductor industry; some global macroeconomic issues will not only affect the semiconductor industry, but also It has a negative impact on the global economy. On January 10, at the "2012 China Electronic Component Industry Innovation and Development Conference" hosted by Huaqiang Electronic Network and "2011 Huaqiang Electronic Network Quality Supplier Award Ceremony", Liu Hui, a senior analyst at Huaqiang Electronic Industry Research Institute, shared " The 2012 Semiconductor Applications Market Hotspot Review and Outlook."

2011 Semiconductor Industry Review and 2012 Discussion In 2011, the global semiconductor industry was flat with hot and cold. The second half of 2010 began to be weak and the peak season was not prosperous. After the earthquake in Japan, Q2 was overstocked, floods in Thailand directly affected PC shipments, Q3 and Q4 cleared inventory, and Christmas orders were conservative. The growth of smartphones and tablet markets was offset by weaker PCs and feature phones.

It is expected that in 2012, the overall industry will remain flat, smart terminals will break out, the macro economy will bottom out second, exports will be weak, and the negative effects of domestic demand will be stimulated. The three major terminals of smart phones, tablets and TVs will be hot, and hardware and software will be upgraded, but the price competition will be fierce. The price does not increase, the white electricity and meter industry are flat, and the margin pressure is high. New applications such as LED lighting still need time, and the price deceleration is faster than the growth of shipments.

Changes and Opportunities in the Semiconductor and Electronics Industry Business Model Real estate increases the cost of physical channels (shop rent/labor); e-commerce channels and operator channels change many eco-industry modes; e-commerce channel threshold is higher and higher Extensive survival; shortening links, reducing channel costs and marketing models are key.

Convergence of global consumer tastes (consistency of traditional media and television vs. Internet); price is very transparent and sensitive (many product pricing is polarized, winners take it all together); emerging markets are long-term focus, but because of multiple purchases, become Become smarter.

In the Internet era, ARM+ Android sweeps three terminals: mobile phones, TVs, and tablets; the convergence of hardware and software in the three terminals, supply chain management is more complex, and vendors are engaged in multiplayer operations; multi-screen interaction and intelligent control are the next hot spots; downstream differentiation becomes more and more. difficult.

In the next 1-3 years, the consumer electronics industry will upgrade the software and hardware to battle. In the next 3-5 years, product consumption, marketing models, and product usage patterns will change dramatically. Liu Hui analyzes that the turning point of the mobile phone in 2011 has already emerged: 1. From 2G functional machine to 3G smart phone; 2. From hardware development to more complex software development; 3. From horizontal division to vertical integration; 4. Winning brand: Either Service brands, or their own brand; 5, the focus shifted from overseas to domestic; 6, from traditional channels to e-commerce and operator channels.

The mobile phone market broke out in 2012, the price war, the total market in China in 2012 was about 300 million, about 40% of smart phones; mature WCDMA technology and terminals, leading the open market; TD open market still needs time.

How will smart phones develop in the future? Liu Hui said that in 2011, WCDMA technology and terminal maturity, about 25M custom market or so, the open market still think that foreign brands, domestic brands for the shop, open market volume depends on operator policies and industrial chain costs, WCDMA open market and exports The market is uncertain, and the winners come from innovative integrated marketing (operators + e-commerce + traditional channels + software applications). After product differentiation and supply chain management and control of millet, Internet companies may still smash dark horses. Traditional channel vendors such as Jinli and OPPO face Great test.

In 2011, the TD market finally took a turn for the better. The 2TD functional machine market took off and the TD semi-open market was the focus. The TD open market still needs time. The technology maturity is more than half a year behind WCDMA, and the TD open market started at the end of 2012. Influx of many manufacturers, operators, e-commerce channels quickly pulled down the retail price. The retail price of the functional machine is 3 times the cost, and the smart machine is 2 times. Everyone wants to occupy the terminal first and then consider the profit.

The domestic chip's outlets for domestic flats and MIDs are expected to exceed tens of millions this year and will double next year: 1. In 2011, shipments of chips will be about 14 million, and terminals will be about 12 million; 2. Exports will account for more than 80%, mainly gifts, Large-screen MP4 market expansion; 3. Shipments of 25 million in 2012, still exporting mainly take off in the domestic market; 4, 7-inch Kindle tablet priced at US$199, bring variable to the industry 5. 1G (1G) in the first half of next year (@ A8/A9) products are the mainstream.

At the same time, the market for tablet and MID chips in 2011 and 2012 is also full of changes. Before the launch of Rockchip 2918, the market window for Telechip and Amlogic switched from 2818 to 2918 in the first half of the year, losing low-end customers to VIA and VIA in the second half of the year. Bringing vitality to Zhongxingwei and Yingfangwei and the rapid rise of Quanzhi. In 2012, Rockchip, Quanzhi, and VIA may dominate the tablet and MID markets. Ruixin won the software and wins the hardware.

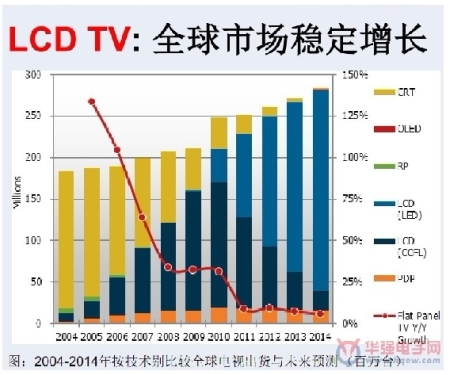

In 2011, China’s LCD TV market reached 40 million units, and Chinese manufacturers accounted for more than 80% of the market. This was a year-on-year increase in Chinese manufacturers' prices, and the prices rose (LED/3D/intelligence). Samsung and LG kept their profit strategies conservatively, and the profits of domestic TV manufacturers increased. In 2012, major domestic brands forecast a 20-30% increase in shipments (about 10% of international brands); Liu Hui said that the global market for LCD TVs has grown steadily. The figure above shows the comparison of global TV shipments and future by technology category from 2004 to 2014. Forecast (million units).

"Home appliances to the countryside, trade-in, energy-saving subsidies," and other policies have gradually withdrawn, and China's white-power market has slowed down. There may be zero or negative growth in the next 2-3 years. Driven by stimulus policies, domestic white-scale enterprises have rapidly expanded their scales in the past two years, channel costs have increased substantially, and their net margins have declined; Rumei's net profit is only 4% or more. Foreign home appliance companies devote themselves to market channels, brand training, technological innovation, and patent maintenance. Domestic companies are at risk of purely processing and manufacturing companies; the widespread adoption of frequency conversion technologies and other technology upgrades provide growth drivers; white electricity is favorable to withdraw, high growth ends, and the future Can be expected.

Finally, Liu Hui analyzed the LED market: the upstream production capacity will grow too fast, and will slow down next year. The production capacity will be released and the price will be further reduced. The large-capsule makers will have stable revenue and overall profits will decline. The growth of applications will depend on lighting and shuffling will be inevitable. Technology to reduce lighting costs, a lot of civilian use takes 3-5 years

Home and indoor or building air filters remove unwanted particles like dust, pollen, pet dander and mold and ensure even the most allergy prone can breathe easily year–round. However, choosing the right filter for your home can be a rather involved process. To help, here are the most common indoor air filters and what each of them provides. The filters are the simplest basic component for air filtration solution through your heating and cooling system ,It is important that you constantly monitor the buildup of debris on these filters as well because it can easily be recycled into the air supply. It is easy change and maintain.

Indoor Air Purification Filter & Air purifier filter

Air Filter, Indoor Air Purification Filter,Building Air Purification Filter,Panel Air Filter

Donguan Bronco Filter Co., Ltd , https://www.broncofilter-cn.com